What is the best term life insurance?

Posted in term life insurance last updated on August 31, 2019

Posted in term life insurance last updated on August 31, 2019

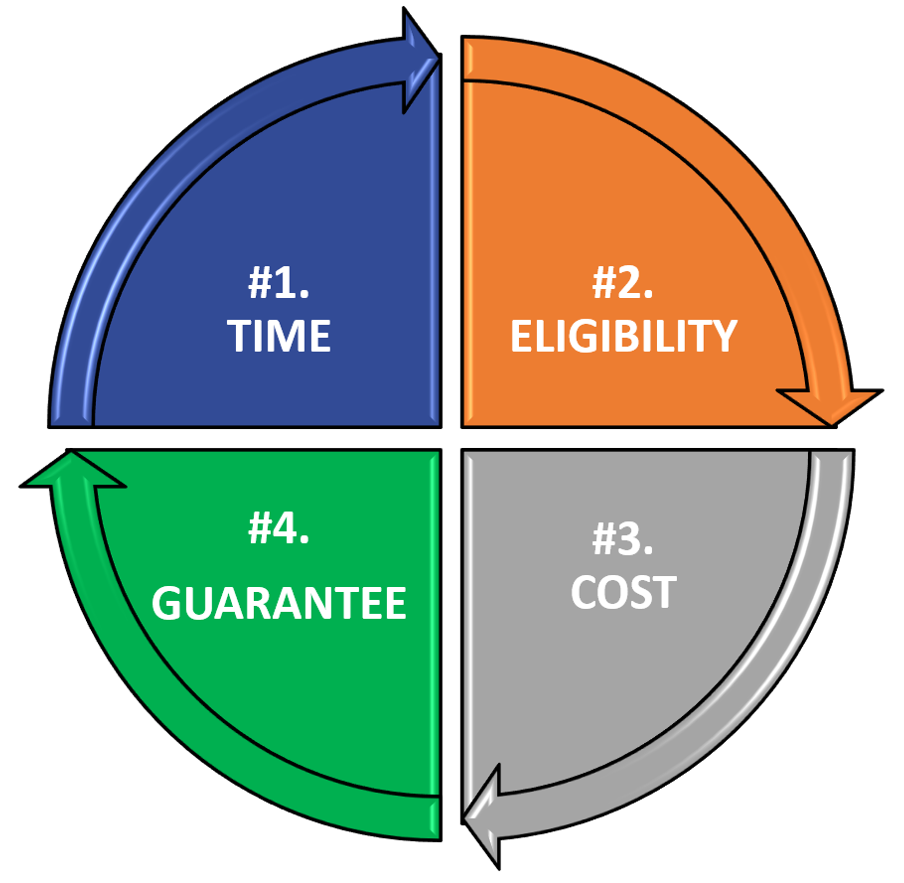

Finding the best term life insurance is like putting a puzzle together. So, you need to match these four parts: eligibility, guarantees, time, and cost to find the best term life insurance for you. The puzzle pieces are unique for each individual. Consequently, the best term life insurance will differ from person to person. Here are how the puzzle parts fit together. The death benefit that a life insurance company pays is through contracts called policies. The agreement states that if you meet the ELIGIBILITY requirements, the insurance company will GUARANTEE to pay to a beneficiary a set amount of money if you die within a certain amount of TIME.

Furthermore, in exchange for this guaranteed payment by the life insurance company, the contract states that you agree to pay a specific COST or premium to the life insurance company. It is that simple. To find the best term life insurance, determine which insurer matches your ELIGIBILITY; has the best GUARANTEE; fits your TIME line, and has a competitive COST.

Put the puzzle parts into questions in this order.

- How do you determine the best number of years or TIME period to have life insurance?

- Which life insurance company’s ELIGIBILITY requirements do you best meet?

- How can you find the best price or COST?

- How can you determine the safety of the life insurance company’s GUARANTEE?

TIME

The length of time that a life insurance policy is structured will change the cost dramatically and perhaps affect your eligibility. So, to find the best duration of a life insurance policy, match the life insurance policy with your needs. Here is an example of how finding the right length of life insurance policy applies. Suppose that you have a thirty-year mortgage. And, your goal is to protect your family’s ability to stay in the family residence if you die within that thirty-year time frame. You would shop for a 30-year life insurance policy to fill that need.

Round up the duration to save money

What do you do if you need life insurance for between 21 and 29 years? You may want to consider quotes on a 30-year term life insurance policy. Why not search for a 25-year term life insurance policy if your need is for between 21 and 25 years? You can search for a 25-year term life insurance policy. But, what you may find is that there are more 30-year term life insurance policies available than 25-year life insurance policies. More life insurance companies have chosen to create a 30-year contract over a 25-year contract. That may change in the future.

Additionally, you may find that the 30-year term life insurance policies are similar in price when compared to the 25-year policies. So, it might make sense to buy the 30-year term life insurance policy. If you do not need the life insurance for the full thirty years, you can terminate the policy at any time. Just notify the life insurance company that you no longer need the policy.

Length of time

The duration of the life insurance policy that you are requesting will affect your eligibility. Most life insurance companies stop offering term life insurance policies past the age of eighty. Hence, if you are sixty years old, and you search for a 30-year term life insurance policy, the quote engine will not provide any options. The period you are requesting goes beyond the age of eighty. If you are sixty years old, looking for term life insurance, the longest policy you will find is twenty years. Unless you find an annually renewable life insurance policy. Annually renewable life insurance policies increase in price every year and can last up to age 95. However, those people holding annually renewable life insurance policies usually cancel them long before the age of 95 because they become too expensive in the later years.

ELIGIBILITY

Every life insurance company has ELIGIBILITY requirements to buy their life insurance policies. The process of evaluating potential customers ELIGIBILITY requirements is called underwriting. And, the person that reviews your application for life insurance coverage is called an underwriter. The first step to consider in finding the best term life insurance coverage is determining which life insurance company’s ELIGIBILITY requirements you fit? Here are some of the ELIGIBILITY requirements that life insurance companies consider: gender, age, your health, and lifestyle habits. Let’s break these four eligibility requirements down more precisely.

GENDER

It is a fact that women historically live longer than men. As a result, with all other factors being equal, life insurance cost for women is less expensive than for men. If you find a life insurance policy that has one rate for men and women, it is usually overpriced for women. Gender-specific life insurance policies have a more competitive cost. Gender is not a significant factor in finding the best term life insurance

AGE

A new life insurance policy that had the best price this year might not be as competitively priced next year. Life insurance companies change their new life insurance rates from year to year to remain competitive. Our life insurance quote engine is designed to find the best price as prices change. However, we manually check each quote. We want to make sure you get the best price on a life insurance policy.

Age is a significant factor in determining the cost of term life insurance. So, as you get older, term life insurance policies will increase in price. There are two methods that life insurance companies use to determine your age. Some life insurance companies do not change the price until the date of your birthday. And, some life insurance companies consider your age within six months of the date of your birthday. For example, if you are applying for a policy on January 1st and your birthdate is on June 1st, the policy would is calculated at the June 1st age in the current year.

An experienced guide makes a difference

Here is where an experienced life insurance agent can save you money. Some life insurance policies allow the policies to be backdated. This tactic would be useful in the previous example. If a policy could be backdated to December 1st of the past year, then the life insurance policy’s cost will be based on the previous birthdate. As you get older, that saving-the-age strategy can save you a considerable amount of money. If you were buying a 30-year life insurance policy, that strategy would save you money every year for the next thirty years.

Term life insurance policies are available with coverage up until age 80. However, if you are over age 50, we will automatically research the best term life insurance over 50. And, we will research permanent life insurance to be sure you are getting the best policy at the best price. Age is a factor in which life insurance companies heavily compete for your business. Accordingly, from age 18 to 50, finding the best life insurance cost changes frequently depending upon competing insurers, life insurance company proprietary strategy changes, the economy, technology, insurer profitability, and insurer losses.

Keeping up with change

A new life insurance policy that had the best price this year might not be competitively priced next year. Life insurance companies change their new life insurance rates from year to year to remain competitive. Our life insurance quote engine is designed to find the best price in those age bands. However, we manually check each quote when working with a client to be sure they get the best price on a life insurance policy.

No-Exam Life Insurance

If you meet the ELIGIBILITY requirements, you might qualify for No-Exam Life Insurance. No-exam life insurance only requires you to answer a few questions about your health and your lifestyle habits. The algorithm life insurance companies use to determine if a person qualifies for No-Exam Life Insurance is complicated. And, each company closely guards its propriety process. However, you can reduce their process down to two simple questions. What is your prescription medicine history, and do you have a good driving record. Meet those qualifications, and you may qualify for No-Exam Life Insurance. This type of life insurance will be one of the first points we discuss when you apply for a life insurance policy with us.

Guaranteed issue for older ages

Once a person reaches the age of 50, the competitive nature of term life insurance begins to narrow. Some companies specialize in covering people from age 50 to 80. So, it warrants shopping for the best cost. If you fall within this age band, we will shop for guaranteed issue life insurance policies too.

Guaranteed issue life insurance is similar to No-Exam Life Insurance. Your health is not an issue. Although, we will need to discuss some of the policies limitations. Depending upon your goal for life insurance, term life insurance may not be the best option. Hence, A permanent life insurance policy with a fixed cost may be a better type of life insurance for people in the older age bands. For more on permanent life insurance policies, check out my other blog post, Which is better, term or permanent life insurance?

Your Health

Your health is a significant factor in applying for term life insurance. We generally categorize customers for life insurance in three ways.

- Excellent Health – If you have excellent health, you may qualify for No-Exam life insurance.

- Better Health – This may mean you have a health issue that is not a significant factor. You may not qualify for No-Exam life insurance. But, that does not mean that you will not be eligible for the lowest COST. How you justify your eligibility is different. Ask yourself a few questions. Have you had any recent doctor visits? Have you had any past speeding tickets? If the answer is yes, then you will need to provide more information. In this situation, you may also need to agree to have your basic health exam, or agree to a blood and urine test. Don’t be discouraged. You can still get reasonable life insurance rates, and the testing is done at your convenience. Plus, it doesn’t cost you anything.

- Improving Health. If you have a significant health issue, we can still help you get life insurance. We excel at finding the best term life insurance for those with health issues. The best way to help people with significant health issues is to have a conversation about your problem and discuss what you need. Accordingly, there is a process of finding competitively priced life insurance for you too. If you have more than one health issue, you can still qualify for life insurance.

Lifestyle Habits

Lifestyle habits can have a significant effect on life insurance cost and availability. Most life insurance companies will increase the cost of life insurance by 50% to 100% for customers that smoke cigarettes or marijuana. However, some life insurance companies do offer lower rates than their competitors. Cigars and smokeless tobacco use may increase cost depending upon the frequency of use. There is a company that will provide customers with non-smoking rates if the customer agrees to stop smoking and be tested for nicotine after twelve months. If the customer still smokes, they will not have their life insurance canceled. However, the rates will increase to smoker rates. If you are trying to stop smoking and need life insurance, this may be a perfect life insurance policy for you.

Is your hobby or job dangerous?

Lifestyle habits would also encompass high-risk hobbies or higher-risk occupations. For example, scuba divers will have higher rates if they dive below a certain depth. Pilots will have lower rates after they have a certain number of hours of flying experience. The general approach for high-risk hobbies and high-risk occupations is being precise about the frequency and extent of either hobbies or professions.

Are you are a good driver?

Lifestyle habits also include driving. So, if you have a higher number of auto accidents, it will affect your cost or eligibility. Plus, if you have three or more speeding tickets, DUI or reckless driving violations; it will affect your price or ability to qualify for life insurance.

It takes extra effort in communicating with a life insurance underwriter about any lifestyle habits. To find the best term life insurance policy in these circumstances, a more experienced life insurance agent can offer several alternatives. Plus, they can be of significant value in communicating with the life insurance underwriter.

Guarantees

The last aspect of finding the best term life insurance is understanding the guarantee that the life insurance company offers. Hence, there are two considerations when it comes to guarantees, one is contractual, and the other is financial strength. The contractual aspect of guarantees concerns the assurance that the premium will not increase. When you are looking for a life insurance policy to be in force for a certain number of years, be sure that you understand how the cost may change. For example, some companies may offer a 15-year guaranteed life insurance policy. But, the guaranteed premium is only five years. This is a point that I have seen some agents overlook.

Look at the details

Be cautious and look specifically at what is being guaranteed. The guarantee could be that the life insurance company is only assuring that the customer will be offered life insurance for fifteen years. However, after five years, the cost can increase. The printed illustrations that you are provided in instances such as this will have a column of the current price, and it shows the premium being level for fifteen years. However, the guaranteed column on the illustration may indicate that the guaranteed premium is only for five years, and then it may increase for the remaining ten years.

Financial strength

The second aspect to consider about life insurance company guarantees is what happens if the life insurance company fails to meet its financial obligations? The first thing to look at for financial strength is to look at the financial ratings for the life insurance company. On this website, after you enter your personal information at one of the orange quote now buttons, you will be provided a list of companies that best meet your needs. Additionally, that illustration will also have a page that compares the financial strength of the life insurance companies.

Don’t let ratings fool you

You may find that the best term life insurance company for you is a lower rated life insurance company. However, another life insurance company with better financial ratings is a few percent higher in cost. At that point, you should communicate with your life insurance agent and ask for their advice. An experienced life insurance agent can help you assess the financial strength of a life insurance company. Also, an experienced agent can help you determine if the lower-rated company that is less expensive or, the higher-rated company that costs more is best for you.

In conclusion, finding the best term life insurance company is simplified by the technology available through websites like Advice4LifeInsurance.com. Although, people’s circumstances vary from person to person, and technology has its limits. The is why we manually check each quote to be sure you are getting the best life insurance at the most reasonable price. The person that guides you through the life insurance buying process can make a significant difference in how much you pay for the life insurance. Plus, especially if you have health issues or a complicated life insurance need, the insurance professional you work with can make benefit you greatly.