Whole Life Insurance vs Term

Posted in whole life insurance last updated on September 8, 2019

Posted in whole life insurance last updated on September 8, 2019

Which is better, whole life insurance or term life insurance? By and large the answer today is the same as it was years ago. The best life insurance depends upon its purpose, your age, health, and budget. Today, we’ll look at what a couple of famous financial gurus have to say about life insurance. In light of their opinions, I’ll share with you two of my client’s experiences from year’s past. Additionally, I will give insight into the structure of the two insurance types.

Dave Ramsey and Suze Orman are two popular financial pundits. Dave Ramsey says, “term life insurance is always the best option,” and life insurance’s “only job is to replace your income when you die.”1 Suze Orman says, “life insurance is an expensive way to invest.” 2 I say that they are both half right.

Being half right?

Rest assured that I agree that many times term life insurance is the best life insurance. That is to say if you have a definitive risk for a specified period. For example, a home mortgage is a perfect illustration. Let’s say that you want to pay off your mortgage in twenty years. So, you buy a life insurance policy that lasts only twenty years. In that case, term life insurance would be perfect for you. Or, let’s say you have a baby. In light of that, you have more financial obligations. You may want to provide money to your spouse and for that child through college-age if you die. Given that, having life insurance for twenty-five or thirty years may be the best choice. In this situation, term life insurance fits well.

By comparison, consider what is the best choice if your time frame changes. Or, think about what you would do if your health and finances change, but you still needed life insurance. Here is what I mean. The best uses of term life insurance and whole life insurance are based on what their name implies. Term life insurance is for a definitive period. If you know you are going to need life insurance for your entire life, whole life insurance is a better option. Whole life insurance can also be the right choice for the death benefit and long-term financial goals. I’ll give you an example of this circumstance in a moment.

My view of the gurus’ opinion

My perspective on Dave Ramsey’s advice is that he is taking an incomplete look of whole life insurance. He is also overlooking many of the uses for life insurance when he says life insurance is only for replacing income. His advice eliminates some people’s circumstances. He is assuming that all people’s needs are neatly organized into time segments.

In contrast, whose life goes exactly as planned? Things in life usually take longer than expected and are harder than you anticipated. I have spoken to many people over the years who bought term life insurance for twenty years. When the life insurance expires, they want the coverage to continue. However, their health has declined, and a new policy is unavailable or extremely expensive.

Be that as it may, if you are young and you have a family, term life insurance is probably the wisest purchase for a limited number of years. If you look beyond a set period and see a need for life insurance, blending whole life insurance is a good option.

If you read the blog post from which the Suze Orman quote was taken, you’ll see that she is referring to guaranteed issue whole life insurance. Orman is emphatic that guaranteed issue whole life insurance is a bad purchase. If you think about that for a moment, you may see that it is a limited view.

Real-life example

I have been a financial advisor for over thirty years. I have helped a lot of people. When I give you a real-life example, I am not using the person’s real name, and the circumstances have been changed a little. I take protecting my clients’ privacy very seriously. With this in mind here is a real-life example of a person that bought a guaranteed whole life insurance policy.

About twenty-five years ago, I sold a twenty-year term life insurance to a client who was in his fifties. Let’s call him Dan for this example. Dan intended that in case he died; he wanted his wife to have enough money to pay off their home mortgage. Twenty years passed and life did not work out the way Dan had expected. Dan was now in his seventies. He had a monthly pension and Social Security. Their family savings were small. Dan was diagnosed with prostate cancer. Luckily it was slow-growing cancer. None the less it was still cancer.

My recommendation

Dan was worried about his wife’s future. So he called me to see if I had any ideas on how they could rearrange their finances. His concern was what would happen when he died. His wife was several years younger than him. If he died, his wife would have a significant financial burden from personal debt and the cost of his funeral expenses. I gave Dan two pieces of advice. First, I suggested that Dan looks at the value of their house. Since they owned the house, they could consider a reverse mortgage that would give his wife a line of credit. Reverse mortgages are a topic for another blog. In short, it fits well into Dan’s circumstance.

Second, I recommended a guaranteed issue whole life insurance policy. Dan’s first response was a surprise. In fact, he could qualify for a life insurance policy in spite of his cancer diagnosis. There was one qualification. The policy would not pay a benefit for the first two years of the policy. If Dan died within the first two years of owning the policy, his wife would only get the return of the premiums paid.

Here is the reality

In reality, the guaranteed whole life insurance fit very well for Dan’s circumstances. Dan was more concerned for his wife beyond two years. So, he purchased the guaranteed issue whole life insurance. Plus, he and his wife applied for the reverse mortgage line of credit.

The way that the line of credit worked, it would provide a financial buffer in case Dan did die within the first two years. Dan’s pension was based on his life and his wife’s life. Consequently, if Dan died before his wife, the pension would be reduced. In this situation, the line of credit provided a source of money that could replace Dan’s pension. Additionally, it would provide enough money for his final expenses.

Basics of a HECM reverse mortgage

Reverse mortgages can be a significant source of income for a retiree. In light of Dan’s circumstance, I’ll only give you a basic explanation of how they work. Here is an essential aspect of reverse mortgages. The reverse mortgage provided money that did not have to be paid back to the mortgage company unless two criteria were met. First, if Dan and his wife died the reverse mortgage would be due. The proceeds from the sale of their house repay the reverse mortgage. The amount payable to the mortgage company can never be more than the sale price of the house. Second, if they moved to another residence the reverse mortgage would be due. Home Equity Conversion Mortgages or commonly referred to as a HECM are a specific type of reverse mortgage that includes these two criteria.

Why whole life insurance works for Seniors

Here is Orman’s complaint about guaranteed issue whole life. If a person lives to their theoretical life expectancy, they would be financially better off putting the money into savings. In light of Dan’s circumstances, he was not expecting to live to his life expectancy. He was concerned about what would happen in the next five to ten years.

In addition, I want to point out that there was not only one dimension to my recommendation for Dan’s dilemma. I am an insurance agent which means I can represent life insurance company products. More importantly; I am a financial advisor. Given that I look at a client’s whole financial situation. If you would like to find out which life insurance would fit you best, you can request a quote any time by clicking on the orange request a quote button.

When is term life insurance the best option?

As I have noted, timing is a crucial consideration when buying life insurance. Term life insurance is life insurance that only pays a benefit when the person insured dies. There is no cash value

Determining cost

The cost of life insurance depends on a person’s age, health, lifestyle, personal habits, and occupation. It is easy for customers to see the cost of life insurance. About half of the people that apply for life insurance can also qualify for no exam life insurance. That means that when some people apply for life insurance, they will not have to submit to a physical exam, give blood and will answer limited questions about their health. You can learn more about no exam life insurance here.

Another real-life example

One of the benefits of being in business for so many years is I have had the opportunity to see how different life insurance policies work in real life. To that end, I’ll direct you to another blog post on how term life insurance worked out for a client. That blog is a story of a husband and wife that were in business together. They bought large term life insurance policies on each other, and the unexpected did happen. You can read that story here.

What’s the difference between whole life insurance vs term

To continue, it is valuable to know the fundamental difference between whole life insurance vs term life insurance. Term life insurance is an agreement between a life insurance company and a customer called an insured. The agreement states that once approved; the life insurance company will pay a cash benefit in the event the insured dies. The agreement called a policy only last for a specific period. Once the period ends, the contract ends, and there is no cash value. The design of a whole life insurance policy is to last the entire lifetime of the insured. Like a term life insurance policy, the whole life insurance policy is an agreement between the life insurance company and the customer, the insured. The agreement lasts the entire lifetime of the insured.

How does whole life insurance work?

Whole life insurance has a build-up of cash value for a future event. That future event is the death of the person that is insured. From beginning to the life expectancy of the insured person money is being set aside. At any time during the life of the insured person, the cash value can be determined. In the beginning, whole life insurance policies are more expensive than term life insurance. Whole life insurance policies may have a cash value available if the agreement is terminated by the insured before their death. The amount of cash available depends on many factors. However, in most instances, the longer the whole life insurance policy is in effect, the more cash value that will be available.

An exception to this would be if the whole life insurance policy were designed to have a death benefit and a cash value that is based on investment market values. Commonly referred to as variable life insurance, this type of life insurance is very complicated, and based on my experience, I do not offer variable life insurance because of its unpredictability. I personally owned variable life insurance and dropped it.

Whole life insurance’s big advantage

One of the most significant benefits to whole life insurance is that the cost of life insurance is guaranteed never to change. You never have to reapply or requalify. As your health changes, the cost of life insurance stays the same. This is a big deal.

In comparison, universal life insurance has a cost of life insurance that can change yearly. In recent years changing premiums and “interest rates caused (universal life insurance) premiums to soar when they were supposed to stay level.”3

Not all whole life insurance is the same

Equally important, there are two types of whole life insurances. The first type is called participating whole life insurance. In brief, policyholders are the company owners in participating whole life insurance. Company profits are passed on to the policy owners.

Consequently, policy owners participate in company profits. This type of life insurance is well suited for people that want to use the cash value as a conservative type of cash accumulation vehicle. It is considered a conservative asset because it has a guaranteed cash value and a guaranteed death benefit. The longer that the policy owner keeps the policy, the higher the guaranteed value increases. If the insurance company has additional profits, they are passed on to the whole life policy owners in the form of policy dividends. As a result, participating whole life insurance policy owners are the owners of the company. This type of life insurance company is called a mutual life insurance company.

The second type of whole life insurance is non-participating whole life insurance. This type of life insurance company is owned by separate stockholders. If there are profits in a stock life insurance company, they are passed on to the stockholders. Stock life insurance companies predominantly are companies that offer senior life insurance policies. In the final analysis, stock life insurance companies are well suited for whole life insurance for seniors. There is more of a focus on the death benefit than the cash value.

Which is a better term or whole life insurance?

At any rate, both types of whole life insurance, as well as term life insurance, have their own strengths and weaknesses. Compared to whole life insurance, the most significant advantage term life insurance has is that it is less expensive when people are young. Generally, if you buy a term life insurance policy before middle age, it is cheap life insurance. For many people, protecting their family or business early in their life is paramount. For this purpose, cheap life insurance is precisely what they need.

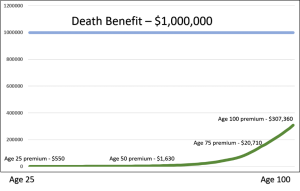

As an illustration, look at the following graph. The blue line is the death benefit of $1 million. The green line is the cost of life insurance. You can see that there is a quick increase in price in the later years. Once a person reaches forty-five to fifty years old, the price tends to increase rapidly.

The long-term cost of life insurance

When is whole life insurance better?

In this discussion, I am referring to participating whole life insurance. If a person is concerned about providing life insurance for their entire life, then participating whole life insurance is better. There is a significant amount of propaganda pushing the purchase of term life insurance because it is cheap life insurance. That may be true for younger people. As shown in the previous example, when an insured goes beyond middle age, life insurance is relatively expensive. Had an older person purchased a participating whole life policy early in their life, it would be much less costly in senior years. Remember, the cost is guaranteed not to increase.

Best time to purchase

In the previous example, the 25-year-old paid $550 compared to the whole life policy costing $8,940. Understandably, that is a big difference. Hence, that is why blending term life insurance and whole life makes more financial sense. It takes a degree of financial maturity as well. At 25, a young person is considering if they will need life insurance beyond the age of fifty. By the age of 70, the term life insurance example shows the cost of life insurance at $20,710. The whole life policy’s price is still $8,940.

In general, participating whole life insurance works best in two circumstances. First, whole life insurance should be kept your entire life. Second, whole life should be bought before midlife. In contrast, there are exceptions to these two circumstances. The multiple uses of dividends allow for customization of the policies. For more on participating life insurance visit my blog the 10 Best Life Insurance Companies. There are four lists. Information on participating life insurance is in the section on whole life insurance.

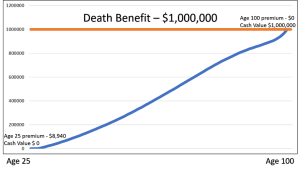

Maximum cash value

The following graph illustrates the lifetime progression of a participating whole life insurance policy. The death benefit is level and guaranteed. However, if the life insurance company has favorable company performance, the death benefit will increase along with the non-guaranteed cash value. The blue line exemplifies the trend that the cash values are guaranteed to follow. Depending upon the design of the policy, there will be a point in the future that the cash value meets the death benefit. This is the endowment point. When a policy endows, it can no longer accept premium payments, and it traditionally pays the cash value to the owner. Life insurance used to endow at ninety or ninety-five. However, with longer life expectancies, most insurers have designed the policies to endow after the age of 100.

cash accumulation in whole life insurance

Cash accumulation in whole life insurance

Term life insurance is a superior choice to buy for a specific number of years and before mid-life. Whole life insurance is better if you want life insurance to cover your entire life, especially in your older years. The deciding factor comes down to what is necessary at the time and will fit into the customer’s budget.

Another real-life example

Here is an example of a client that bought a participating whole life insurance policy for his daughter in 1991. As I have said earlier, when I give you a real-life example, I am not using the person’s real name, and the circumstances have been changed a little.

This is a circumstance where a father wanted to buy a life insurance policy for his twenty-year-old daughter. For this example, let’s call the dad Oscar and call his daughter Amanda. Oscar paid $1400 per year for $205,000 of life insurance for Amanda. Amanda was twenty years old and had a one-year-old child. Oscar wanted to buy life insurance on his daughter to benefit his grandson in the event of Amanda’s death. He purchased a cash value whole life insurance because after Amanda’s son was grown. Oscar wanted the cash value to be available as a gift to Amanda.

Fast forward from 1991 to 2019. Oscar has since passed away. Amanda’s son is grown. Amanda and her husband are buying a home that they can retire to, and they are using the cash value of the life insurance policy as part of the purchase. Below are the results of the policy after twenty-eight years.

A real-life example of a participating whole life insurance policy

- Life insurance beginning date: 1990

- Annual premium: $1400

- Years paid: 28 years

- Beginning death benefit: $205,000

- Date surrendered: 2018

- Life insurance at surrender: $338,000

- Cash surrender value: 88,000

- Rate of return on premium: 5.46%

Even though this is life insurance, the disclaimer told clients about investments is true here as well. The past performance is no guarantee of future results. Future returns on premium are significantly affected by the current low-interest rates. However, cash values for participating whole life insurance companies are dependent upon the insurer’s business performance.

What is the right time to buy life insurance?

If you have someone in your life that will suffer financially if you die, that is when you need life insurance. As we go through life, obligations change. When you recognize those obligations, that is the time to buy life insurance. The key to finding the best time to purchase life insurance is not to wait until it is too late. Buying life insurance is not something that you do for yourself; it is something you do for the ones you love. Click on the orange quote now button to get a quoted and get started.

References

1 “What Is Whole Life Insurance?” Ramsey Solutions. Last modified January 24, 2019. https://www.daveramsey.com/blog/whole-life-insurance

2 Orman, Suze. “Is Life Insurance a Good Investment?” Suze Orman Media. Last modified July 18, 2019. https://www.suzeorman.com/blog/Is-Life-Insurance-a-Good-Investment

3 Scism, Leslie. “Universal Life Insurance, a 1980s Sensation, Has Backfired.” WSJ. Last modified September 19, 2018. https://www.wsj.com/articles/universal-life-insurance-a-1980s-sensation-has-backfired-1537368656